During the past 2 years many crypto index funds emerged as a result of the increased interest in the crypto market. These products offer to their investors a basket of cryptocurrencies under the promise of higher risk-adjusted returns due to portfolio diversification.

In this research article we show how this is actually far from the truth. We find in fact that cryptocurrencies are highly correlated, offering no portfolio diversification benefit by investing in a basket of them. In particular, we find that the performance of Bitcoin and an equal weighted or notional weighted crypto basket portfolio is essentially the same during the analyzed period. Therefore, investors looking for an actively managed product in the crypto space should look at other options, such as a systematic crypto investment program.

A Crypto Index Fund is a product that provides investors an exposure to a basket of cryptocurrencies. The typical methods used to weight the basket constituents are the following:

The main benefits that could potentially be achieved in a basket of cryptocurrencies is portfolio diversification if the constituents are uncorrelated. On the other hand, an investor usually has to pay higher costs compared to a direct investment in cryptocurrencies. These expenses include transaction costs to rebalance periodically and management and sometimes performance fees to the sponsor of the crypto fund index.

In the next section we see if it is worth paying these higher costs analyzing the correlation in the major cryptocurrencies constituents of such portfolios.

Usually proponents of crypto index funds cite portfolio diversification as the main factor in considering an investment in their product. Based on Modern Portfolio Theory, an investor can achieve benefits from portfolio diversification if he invests in a basket of uncorrelated or inversely correlated products.

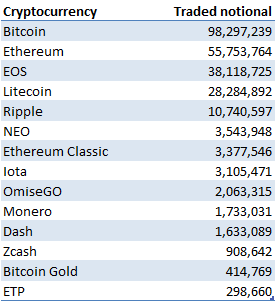

In this analysis we consider the top 14 cryptocurrencies by traded notional on Bitfinex as of April 13, 2019. The period covered goes from March 2013 to April 2019.

Table 1 shows the top 14 cryptocurrencies by traded notional considered in this analysis.

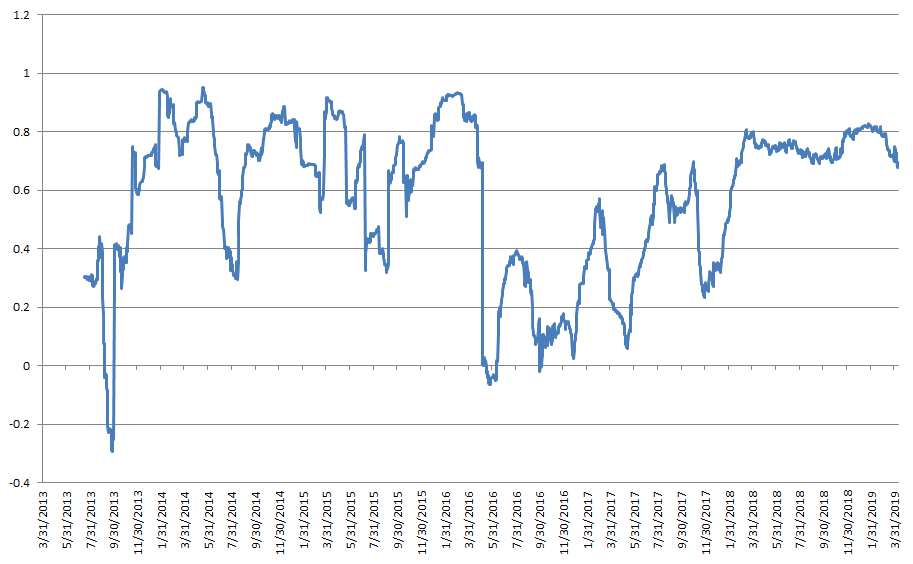

Figure 1 shows the average rolling correlation among the considered cryptocurrencies. As it can be seen from it, cryptocurrencies are highly correlated, with an average correlation of 0.7 as of April 2019. This poses in question the potential benefit that can be achieved through portfolio diversification by investing in a basket of cryptocurrencies through a crypto index fund.

The next section will analyze if this is true by comparing the performance of one cryptocurrency, Bitcoin, to a crypto basket and see if they are similar.

Figure 2 shows on a log scale the hypothetical performance of 2 crypto index funds, equal weighted and notional weighted, compared to a passive investment in Bitcoin. The figures for the crypto funds are gross of transaction costs and fees charged by the sponsor. The performance of the crypto fund indices will be actually lower after considering them. As the figure shows, the performances of the 3 portfolios are very similar.

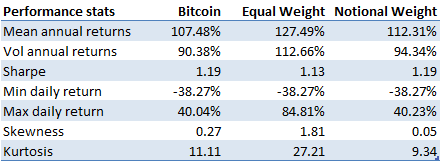

Table 2 shows the performance stats of the 3 portfolios to compare them in a more rigorous way. As the Table show, they all have similar levels of returns, volatility, and Sharpe ratio accordingly.

Table 3 displays the correlation matrix between the 3 portfolios. As we would have expected from our previous correlation analysis on cryptocurrencies, the 3 portfolios are highly correlated (ρ = 0.9), posing in serious doubt the validity of an investment into crypto index funds.

As we have seen from the previous data, crypto index funds cannot provide any benefit compared to a passive investment in Bitcoin. Therefore, an investor looking for an actively managed product in the crypto space should consider other options. An example is a systematic crypto hedge fund, which could potentially deliver alpha and an uncorrelated performance compared to Bitcoin and other cryptocurrencies in both bull and bear market conditions.

From our analysis we can deduct the following key takeaways:

This article analyzes the cryptocurrency market capitalization for the top 20 cryptocurrencies. In particular, it shows the composition of market cap by cryptocurrency, how it evolved over time, and how it compares to traditional asset classes like stocks and bonds. The research finds the following:

The article is structured as follows. The first section analyzes the market cap composition for the top 20 cryptocurrencies over time. The second section compares the crypto market cap to traditional asset classes. The final section concludes.

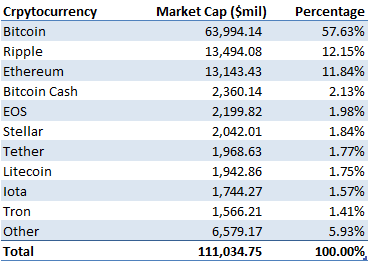

Table 1 shows the top 20 cryptocurrencies by market capitalization considered in this research.

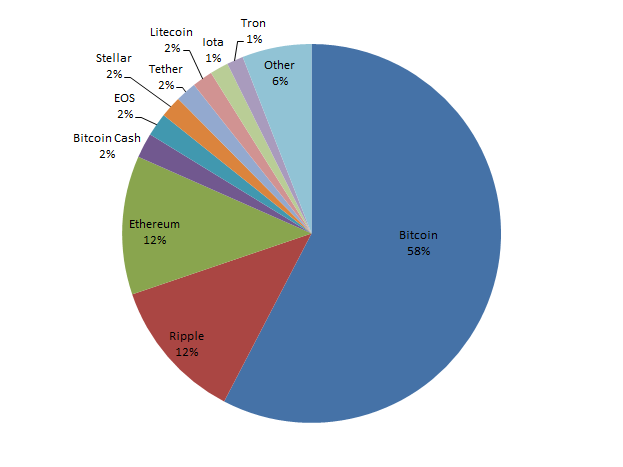

As the figure shows, the current total market cap for all the cryptocurrencies is around $111 billion. Figure 1 shows the distribution of the crypto market cap for the top 20 cryptocurrencies. As it can be seen from it, over 80% of the total market cap is in the top 3 cryptocurrencies, with Bitcoin having 57.63% of the total.

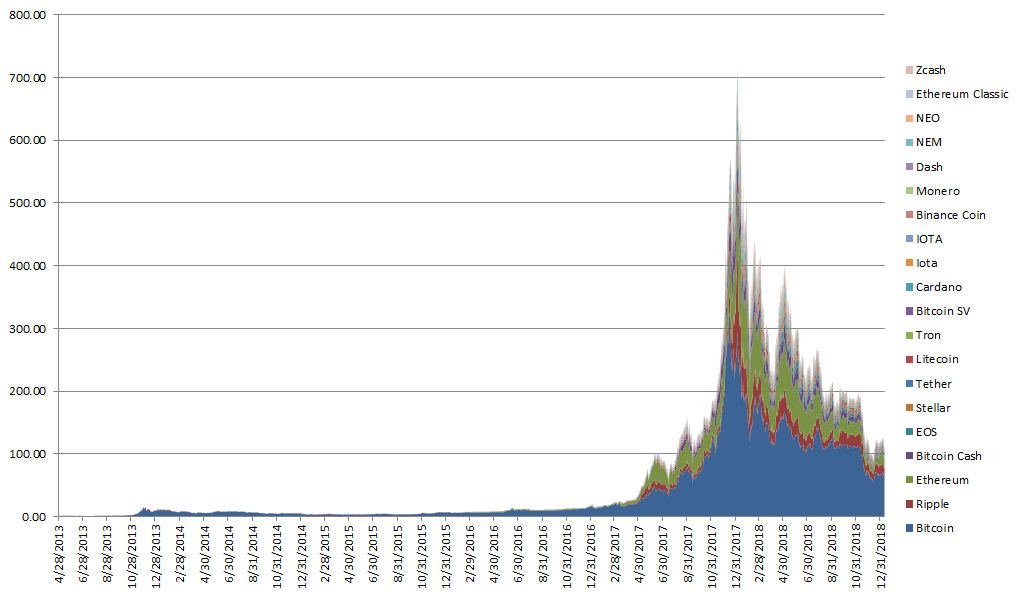

Figure 2 shows the evolution of the crypto market cap in billion of US dollars over time.

As it can be seen from it, the cryptocurrency market cap is very volatile, in a similar way to the crypto prices. It went in fact from around $1.5 billion in April 2013 to $111 billion in January 2019, an increase of around 100 times in almost 6 years.

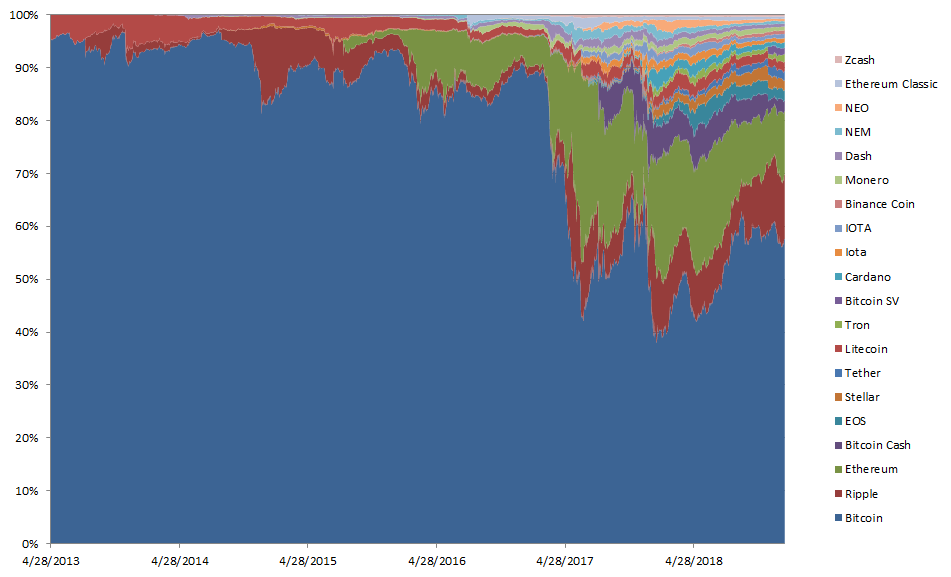

Figure 3 shows the composition of the market cap by cryptocurrency.

As the figure shows, Bitcoin lost its dominant market share during the analyzed period, going from around 95% of the total market cap in April 2013 to around 57.63% in January 2019. Cryptocurrencies that have been quite successful are Ethereum, used in ICO through ERC-20 tokens, and Ripple. Both in fact have managed to achieve around 12 percentage points in market share during the analyzed period.

The next section puts the crypto market cap into perspective by comparing it to traditional asset classes.

Figure 4 shows the market cap of Bitcoin and cryptocurrencies compared to traditional asset classes.

As the figure shows, despite their tremendous growth in the past 6 years, cryptocurrencies and Bitcoin still have a very small market cap compared to traditional asset classes. In particular, their market cap is still lower than Amazon, currently the largest publicly listed company by market cap in the US stock market.

This data shows that crypto is an emerging technology that has the potential to become a new asset class, but it still has a relatively small market cap.

Crypto is a new technological innovation that has experienced tremendous growth in the past 6 years in terms of market capitalization. Nonetheless, it is still quite small compared to traditional asset classes like equity and bonds. We will probably need another 5 to 10 years before considering crypto a relevant asset class in terms of market capitalization.

On December 7, 2018 Bluesky Capital was invited at the Equities Leaders Summit at the Trump National Doral Miami to discuss the adoption of cryptocurrencies as a new tradable asset class from equity investors. The following key takeaways emerged:

• There are still too many risks for institutional investors to enter in the crypto space, including regulatory, reputational, custody, and counterparty risks.

• Cryptocurrencies as an uncorrelated asset class provide benefits to equity or other investors in terms of portfolio diversification

• Crypto is a highly volatile asset class, creating opportunities for hedge funds that employ trend-following / CTA strategies

• The benefits offered by the blockchain technology and cryptocurrencies imply their mass adoption in the next 10 to 20 years

• High fragmentation and scarce liquidity on exchanges create profitable opportunities for hedge funds that use market making and statistical arbitrage strategies by providing liquidity across crypto exchanges

Below are the key takeaways from the conference.

Cryptocurrencies have 4 main risks still too high for institutional investors:

Some hedge funds, especially more nimble ones that manage investments from HNWI’s and family offices, have already decided to assume and possible mitigate those risks with appropriate measures and take advantage of the opportunities created by the volatility present by cryptocurrencies. We anticipate that more institutions will enter the cryptocurrency market in the next 3 to 5 years, when there will be more stability and development in the space and a reduction in the previous risks as a consequence.

Historically cryptocurrencies have been uncorrelated to equities and fixed income. This means that equity or other investors who allocate to crypto as a new asset class can obtain portfolio diversification benefits by achieving lower risk for the same level of expected return or higher expected return for the same level of risk.

Cryptocurrencies are highly volatile, with an average annualized volatility of Bitcoin around 100%. This presents high risks, but at the same time big opportunities for professional investors who adopt CTA / trend-following strategies which generally perform very well in these market environments. The crypto space is highly similar to the futures market in the 80’s or 90’s, which was very volatile and almost no institution wanted to invest, while nowadays is one of the most actively traded and liquid market across all asset classes.

We believe that there has already been too much investment by big institutions and corporations in the blockchain technology and there are many benefits in adopting cryptocurrencies in terms of speed of payment processing to let it go away. The industry is still very new, in a certain way very comparable early stage of the Internet era in the 90’s, where a new technology was brought but people still had to figure out the real potential and new applications of the technology. We believe that complete adoption of blockchain and cryptocurrencies is an inevitable long-term process, which similarly to Internet will probably take between 10 to 20 years to complete.

The crypto market is currently highly fragmented, where one cryptocurrency trades on at least a dozen exchanges, and characterized by a lack of institutional liquidity. These creates profitable opportunities for hedge funds and proprietary trading companies who employ market-making and statistical arbitrage strategies that can collect spreads by providing liquidity on multiple exchanges. At the same time, only a few companies have so far entered the market because of the expertise needed and the substantial investment in technology to operate such activities. We believe that more liquidity providers need to enter the market in order for institutions to consider trading cryptocurrencies without having a meaningful market impact and substantial transaction costs as a consequence.

On December 6, 2018 Bluesky Capital was invited at the Art Decentralized conference during the Art week in Miami to discuss the application of blockchain technology, in particular tokenization, to the art industry. The following key takeaways emerged:

• Tokenization has the potential to attract lots of interest in the art industry as an investment in a new asset class in terms of portfolio diversification

• A regulatory framework needs to be developed to define what a token represent on a legal standpoint and provide more investment confidence for accredited and institutional investors

• Art owners will be able to liquidate portions of existing collections through tokenization

• Accredited investors will be able to invest in art funds who invest in tokenized art and achieve exposure to art as an uncorrelated asset class compared to equity and fixed income

Below are the key takeaways from the conference.

Tokenizing a piece of art consists in creating a dividing the ownership of a piece of art in multiple pieces through the issuance of a token linked to that piece, which is then purchased by multiple investors. This process is equivalent to an equity investment in a company, where multiple investors buy different shares in a company.

This technology has several benefits and opens up new opportunities in the art space, among which:

The technology itself does not guarantee the authenticity of a piece of art itself, which is a work that still needs human experts at the beginning. The blockchain technology in fact only allows the storage of the information regarding a piece of art, such as its provenance, author, etc., on multiple databases (ledger). If the initial information stored in the blockchain technology is misleading or counterfeited, all the subsequent records stored on multiple computers will be as well. This is a process analogous to garbage-in garbage-out (GIGO). On the other hand, once an initial expert has validated that a piece of art is actually authentic and has stored that information in a ledger, it is very difficult to tamper that information.

Tokenization is a new technology, so regulation still needs to keep up with it. Most likely tokenizing a piece of art and selling it to multiple people as an investment configures in a similar way to an equity share in a company, so it will probably fall under security laws and be regulated by the SEC.

Since selling tokenized pieces of art is similar to an offering of securities, in the United States they are usually conducted as a private offering to accredited investors under the exemption of Rule D. Another possibility is to invest in an art fund, which pools money from multiple investors with the purpose of getting an exposure to art as an asset class of to generate a return above a specified benchmark in the sector.

For now it is difficult for retail investors to participate in tokenized pieces of art mainly because of a lack of regulation in the sector and absence of art exchange where tokens can be freely traded. It is possible that in the future, when both regulation and technology will develop for this sector, retail investors will be able to own a fraction of an expensive piece of art like a multi-million dollar Picasso painting by freely trading them on exchanges or investing in an art mutual fund.

Currently artists are happy about the technology since it provides an alternative way to monetize their works of art and potentially sell their works directly to consumers, bypassing galleries, art dealers, and auction houses. It is important to underline that the greatest reward will be probably taken by famous artists who sell pieces worth millions of dollars, since the process of tokenizing and monetizing a piece of art as a form of investment makes sense only for expensive works.

We believe that the great potential offered by tokenization to create liquidity in an illiquid asset class, the low correlation of art as an asset class compared to equity and fixed income, and the low returns delivered by traditional asset classes will potentially attract substantial interest from institutional investors in art as an asset class in an optics of portfolio diversification.

Credit to Light Node Media for organizing the conference.