Recently many people in the crypto space have been talking about the China crackdown on crypto mining and consequent drop in the Bitcoin hashrate. But what is it exactly? In the first part of this article we explore in detail what is the Bitcoin hashrate, and present an analysis of data related to it to discuss its main characteristics and evolution over time. In the second part, we focus on the impact of the Bitcoin hashrate on the profitability of a crypto mining operations, and why miners should pay close attention to it and possibly hedge the hashrate risk with customized contracts or through an experienced crypto asset manager. The final sections concludes with key takeaways.

Bitcoin hashrate refers to the number of hashes computed by all the miners in the Bitcoin network over a period of time and it is measured in number of hashes per second.

In order to process the transactions on the Bitcoin blockchain, miners on the network need to perform a huge amount of calculations to validate a particular block. These calculations consist in computing hashes on a block’s header, and if that is correct, the first miner to do will receive a specified amount of Bitcoin. This is an award created to incentivize miners to invest capital in the mining operation and cover their fixed and operational costs.

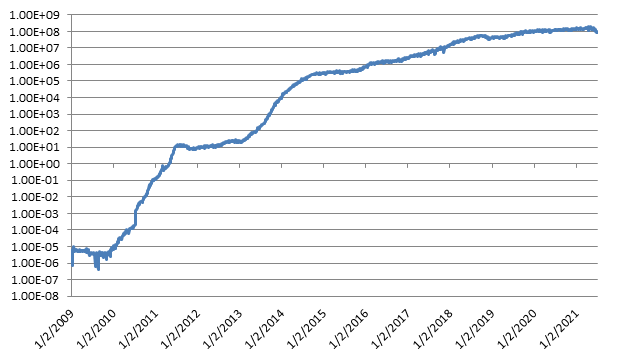

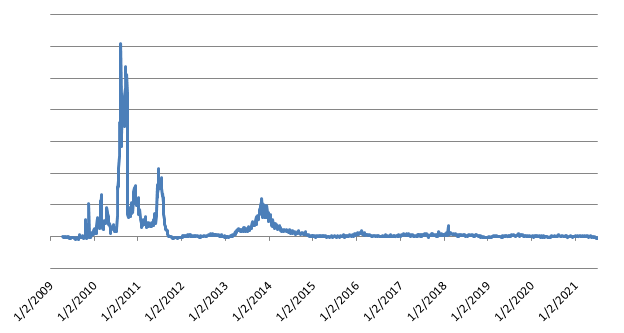

Figure 1 shows the Bitcoin hashrate over time since 2009. As we can see from it, the hashrate exhibited positive but declining growth rate over the years. This may be due to an increase in the number of professional competitors diminishing the profit revenues for each single miner and making mining a less profitable business. Another main reason could be due to the process of Bitcoin halving, discussed in more detail later in this article, where the amount of Bitcoin given to miners as an award for validating the transactions on the blockchain reduces by half approximately every 4 years.

The Bitcoin hashrate is measured in hashes per second (H/s). The current Bitcoin hashrate is about 93 EH/s, where 1 EH is 1018 hashes. Its order of magnitude depends on the number miners in the network and capacity of each one. Table 1 below reports some hashrate units relevant to the hashrate measure.

In order to determine if a hash guessed by a miner is correct, he must check if its value is lower than a positive number called nonce. The nonce represents the difficulty on the network on validating a block. If the nonce is high, it will be easier and more likely to find a lower number than it, while if it is lower the opposite will happen.

The difficulty is adjusted every 2016 blocks (every 2 weeks approximately) so that the average time between each block remains around 10 minutes.

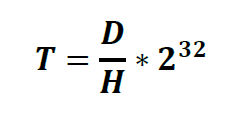

The number of Bitcoins given to miners must be approximately constant over a period of time, and the number of miners is an exogenous variable that is not controllable since anybody can participate in crypto mining anywhere in the world with no restrictions. Therefore, the Bitcoin network automatically adjusts its difficulty to guess the correct hash by changing the nonce. This is done over a number of blocks so that the network can identify a permanent change in the number of miners. The entire process can be exemplified by the following formula:

Where:

T = time to process 1 block on the Bitcoin network (approximately 10 minutes on average)

D = difficulty of the network

H = hashrate,

The hashrate is proportional to the number of miners in the network and the processing power of each miner. As we can see from the previous formula, the higher the network hashrate, the higher will be the difficulty to keep the average processing time constant.

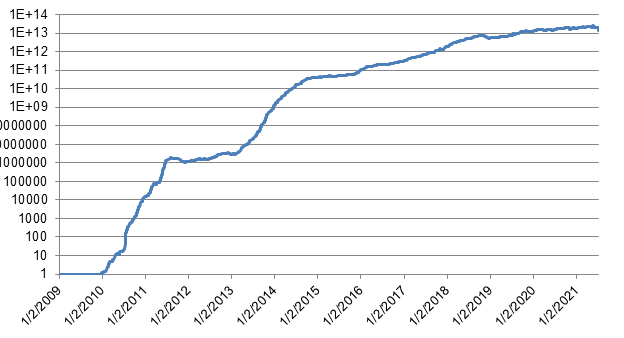

Figure 2 shows the Bitcoin network difficulty over time. As expected from the previous formula, it proportional to the network hashrate, with a correlation ratio of 0.99. This is done to keep the average verification time constant.

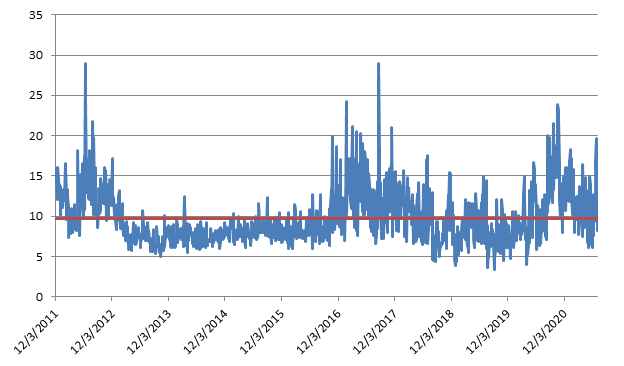

Figure 3 shows the median time to process one block on the Bitcoin blockchain. As we can see from it, the long-term average is about 10 minutes, as expected. We also notice that there are periods of time where the processing time is significantly longer. This is due to a combination of multiple factors, among which the level of congestion in the network due to an increase in the number of requests to be processed, reduced hashrate because some miners may be leaving the network and a difficulty that still hasn’t adjusted to take that into account.

In particular, this explains the temporary increase in processing time in the Bitcoin network and corresponding decrease in difficulty after the recent crackdown on Bitcoin mining in China. This in fact caused a reduction of around 50% of the network hashrate, with corresponding change in the previous numbers.

A higher hashrate should improve the security of the blockchain. Assuming in fact that each miner has a limited amount of capital that he can invest into its mining operation, the hashrate is therefore proportional to the number of miners. Assuming also that these miners operate without collusion, the chances of a 51% attack where one miner can control the blockchain network and reverse the transactions will be lower.

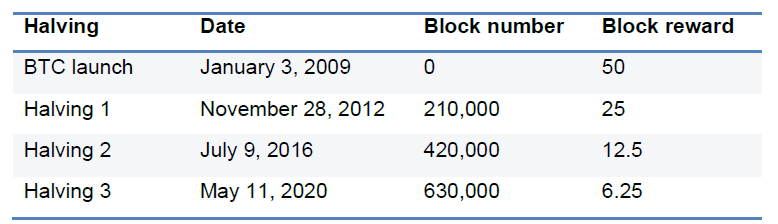

Bitcoin halving is mechanism built in the Bitcoin blockchain network which automatically reduces the Bitcoin reward given to miners to keep the supply of Bitcoin limited. In particular, halving as the names suggests reduces by half the reward every 210,000 blocks, which occurs approximately every 4 years.

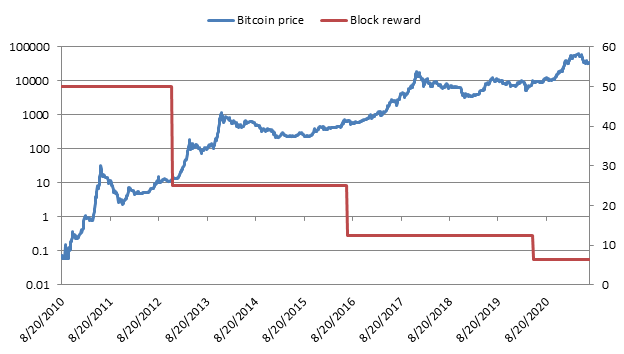

Bitcoin halving it’s very important for miners because it directly impacts their revenues. In fact, each time that a Bitcoin halving happens, their revenues in Bitcoin terms is effectively cut in half. Theoretically since the supply of Bitcoin will reduce, the price of Bitcoin in USD terms should go up assuming constant demand, keeping the mining revenues in USD around the same. We can see if that has been the case over the past years.

Table 2 shows the history of the Bitcoin halving dates happened so far, while Figure 4 shows the Bitcoin block rewards together with the corresponding Bitcoin price. As we can see from it, it seems that there is an increase in price in Bitcoin every time there is a halving. This is consistent with what we predicted before due to the reduction in the supply of Bitcoin and the amount that miners can sell in the market.

Having previously discussed the Bitcoin hashrate we now turn our analysis on how it matters for miners. We have seen that the hashrate is a measure of the amount of competition among miners, since the total amount of Bitcoin produced in a given period of time is kept approximately constant endogenously by the blockchain algorithms.

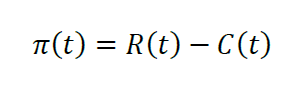

We can decompose the net profit of a Bitcoin mining company into revenues and costs. For our current discussion, we assume that the miner wants to maximize its profitability in USD, since he will have to pay fixed and recurring expenses in fiat currency. Accordingly, we have the following:

Where:

π(t) = profit of the Bitcoin mining operation in USD

R(t) = revenues of the Bitcoin mining operation in USD

C(t) = total cost of the Bitcoin mining operation in USD

In the next sections we analyze each component in more detail, with the corresponding risk for the miner, and determine the optimal hedging strategy.

Bitcoin annual mining revenues in USD are determined by the amount of Bitcoin earned over the year, multiplied by the price of Bitcoin. Assuming that the miner earns a constant amount of Bitcoin each day, and that he sells or hedge immediately them as soon as they are earned, we have the following relationship:

Where:

Rt) = Bitcoin miner revenue on day t in USD

p(t) = BTC/USD exchange rate on day t

q(t) = quantity of Bitcoin earned by the miner on day t

In addition, the quantity earned by the miner is proportional to how powerful is mining rig is, and the total amount of mining competition in the Bitcoin network. This can be expressed as:

Where:

MH(t) = miner hashrate

NH(t) = Bitcoin network hashrate

Combining the previous terms, we have the following expression giving the revenues of a Bitcoin miner on a given day:

As we can see from it, Bitcoin miner revenues on a given day depend on 2 main exogenous variables, the price of Bitcoin and the total network hashrate. In order to minimize the revenue risk in USD terms, it is important to understand the amount of risk present in the previous factors, how much the miner is willing to tolerate, and the best hedging program to minimize them.

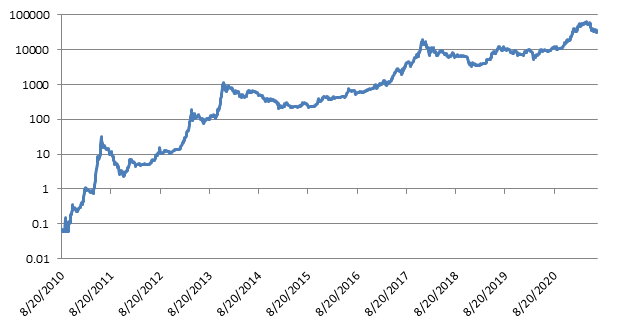

Figure 5 shows the price of Bitcoin since 2010. As we can see from it, Bitcoin is very volatile, with an average volatility of around 150%. Leaving a Bitcoin earning unhedged in USD terms it would therefore be too much even for the most risk tolerant miner. It is in fact so risky that he may even not be able to pay its variable costs denominated in USD terms or other fiat currency. It is therefore important that the Bitcoin miner devises a customized hedging strategy with a professional crypto asset manager to reduce its revenue risk due to the price of Bitcoin.

Figure 6 shows the historical monthly growth of the Bitcoin network hashrate since inception. As we can see from it, it has been growing steadily in the past, at a median rate of 37% per month. This indicates a constant increase in the mining competition and a consequent reduction in the quantity of Bitcoin earned by an individual miner assuming no increase in its mining capacity.

In terms of risk on the miner profitability, the hashrate risk is minor to the price one as being more stable and predictable, but it still accounts for a considerable portion of the Bitcoin miner revenue. This could have negative effects for the mining profitability and success in the long-run. Therefore a proper hashrate hedging program minimizing its risk needs to be devised.

There are currently 3 main ways to reduce the hashrate revenue risk for a miner:

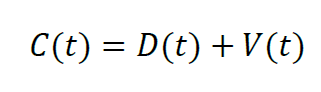

After analyzing the Bitcoin miner revenues, we now turn our attention to the other side of the equation, or the costs. Mining costs can be broken down into the depreciation cost of the initial fixed capital investment, and variable operational costs to keep the mining operation running. In other words, we have the following:

Where:

C(t) = total Bitcoin mining cost in period t

D(t) = depreciation cost mining equipment in period t

V(t) = variable operational mining expenses in period t

The previous 2 costs are contrasting, since an initial investment in higher capacity and modern equipment will most likely result in lower energy consumption. Assuming that the it is optimal for the miner to buy the latest mining technology available on the market because of the gain in efficiency and reliability it can provide, the main focus will then be on the variable running costs.

Bitcoin mining rigs are made by ASIC equipment that is optimized for computing hashing operations very quickly and efficiently specifically for Bitcoin. They work by consuming electricity and producing heat and hashes outputs. Their capacity is given by their hashrate and is measured in hashes per seconds. A current Bitcoin ASIC miner has a hashrate of about H/s.

When considering the running costs of operating these miners, the main factors we need to consider are the electricity, cooling, labor, and storage costs. This is summarized as follows:

Where:

V(t) = total variable costs at time t

E(t) = electricity costs at time t

CO(t) = cooling costs at time t

L(t) = labor costs at time t

S(t) = storage costs at time t

Of the previous costs, electricity is typically the highest and most important one, since this equipment constantly consumes a lot of it to run 24/7. It is also important to note that all of the variable mining costs depend on the location of the Bitcoin mining operation. It is therefore important to perform a thorough initial business plan and feasibility analysis to make sure that the miner will select the optimal location globally depending on its specific constrain.

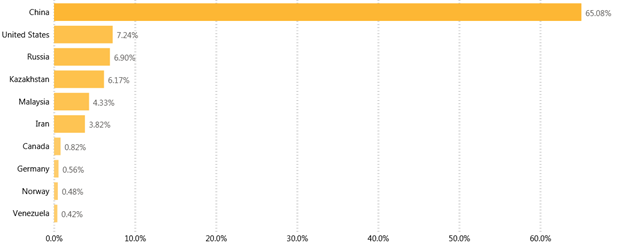

Figure 7 shows the distribution of the Bitcoin network hashrate around the world as of Q2 of 2020. As we can see from it and as reflected by recent data in hashrate drop of about 50%, most of the mining facilities were operating in China, followed by the United States and Russia.

This is mostly likely due to the previous considerations in terms of operational costs, technological advances, and a general interest in the crypto space in the previous countries. Following the recent China crackdown on mining from regulators, we expect that the US will occupy a much bigger share of mining operations for the reasons previously considered.

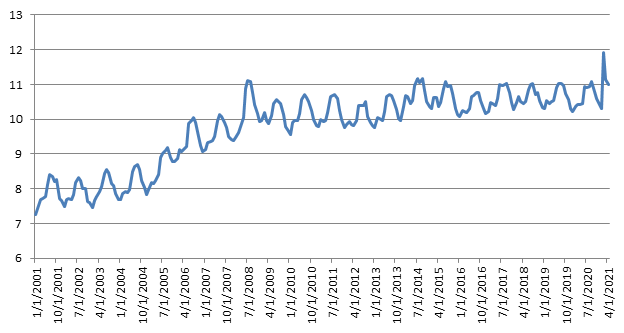

Having understood that electricity is the most relevant variable cost in a Bitcoin mining operation, it is now important to see its volatility and if a miner can reduce the risk in his profits by hedging it. For simplicity and availability of public data, we will use the United States as the place of reference.

Figure 8 shows the commercial price of electricity over time in the US since 2001. As the figure shows, there is some slight upward constant trend and a seasonality component over the course of the year. Based on the previous data, electricity prices seem quite stable over the course of the year, and it is therefore not necessary for a miner to hedge them. The most important decision remains then at the beginning to locate the most optimal region providing the lowest operating variable costs, including electricity.

Having analyzed both the revenues and the costs in depth, we can conclude the following: