By Andrea Leccese

April 16th, 2019

Many crypto hedge funds were launched in the past 2 years because of a significant interest growth in cryptocurrencies. While some of these funds include experienced teams coming from other hedge funds, many of them were actually setup to make a quick profit during the hype.

In this article we will show why most so called crypto hedge funds are not actually hedge funds, but just passive investors in a basket of cryptocurrencies, in a way similar to mutual funds. Despite this, many of them still charge the typical 2/20 management and performance fees typical in the hedge fund world. The first section will introduce crypto hedge funds, while the second one will analyze their aggregate performance by looking at the Eurekahedge Cryptocurrency Hedge Fund Index. The last section concludes with key takeaways.

Crypto hedge funds stats

A crypto hedge fund is a pooled investment vehicle from multiple investors with the purpose of delivering uncorrelated returns with the crypto market by investing in cryptocurrencies. Cryptocurrency hedge funds are actively managed products, with the purpose of generating superior risk-adjusted returns uncorrelated with the direction of the crypto market (alpha). This is in contrast to crypto index funds, which are passively managed product with the aim of delivering just an exposure to the crypto asset class (beta).

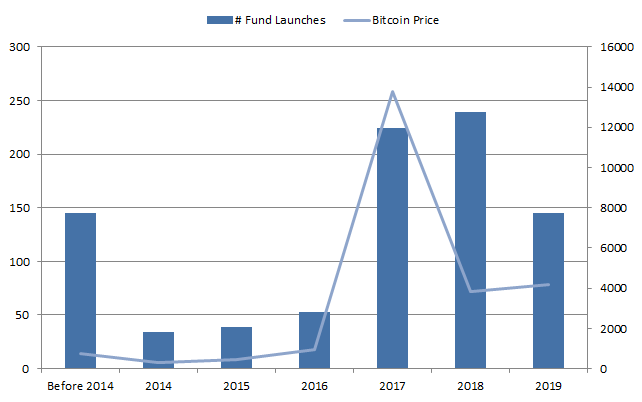

Figure 1 shows the number of crypto fund launches, together with the price of Bitcoin. As it can be seen from the figure, there is a high correlation (ρ = 0.70) between the 2 measures. This should be expected, since a higher price of Bitcoin indicates creates greater interest in the crypto space and possibly higher capacity for crypto funds, with consequently greater economic incentives to launch one.

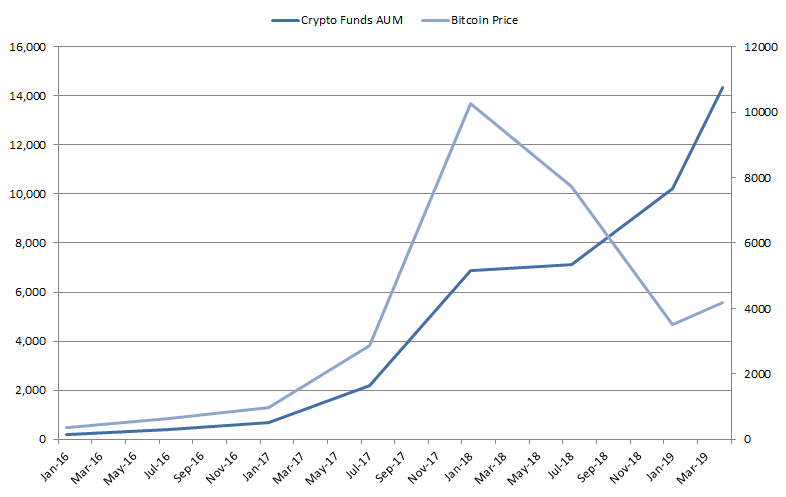

Figure 2 shows the assets under management (AUM) for crypto hedge funds over time, compared to the price of Bitcoin. It is interesting to note that, despite the bear market of 2018, crypto hedge funds still managed to attract capital. This may be due to a general interest in the crypto space, where investors may want to invest for the long term.

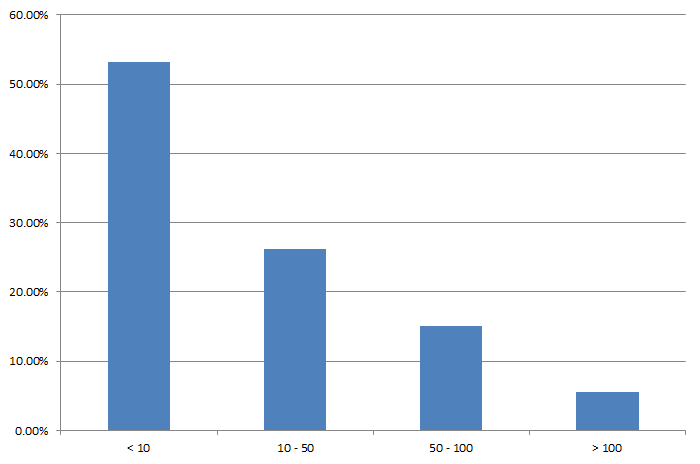

Figure 3 shows the distribution of AUM for crypto hedge funds. As it demonstrates, crypto funds are much smaller to traditional hedge funds, with most of them having less than $10 million in AUM, and only 5% surpassing the $100 million mark.

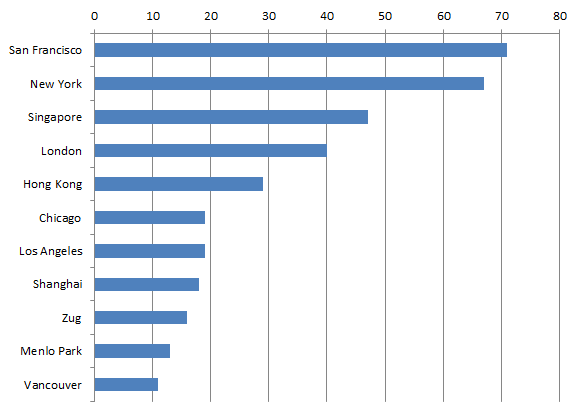

Figure 4 shows the distribution of crypto hedge funds by city. As it can be seen from it, they are dispersed across the globe, with a prevalence in major financial and tech hubs like San Francisco, New York, London, and Singapore.

Performance attribution crypto hedge funds

We now analyze the performance of the crypto hedge fund industry as a whole to see if they provide uncorrelated returns to the markets (alpha), as they should, or if they just repackage passive cryptocurrency returns (beta). In this analysis we use the Eurekahedge Cryptocurrency Hedge Fund Index to represent the performance of a typical crypto hedge fund, and Bitcoin to represent the cryptocurrency market. The analyzed period goes from June 2013 to April 2019.

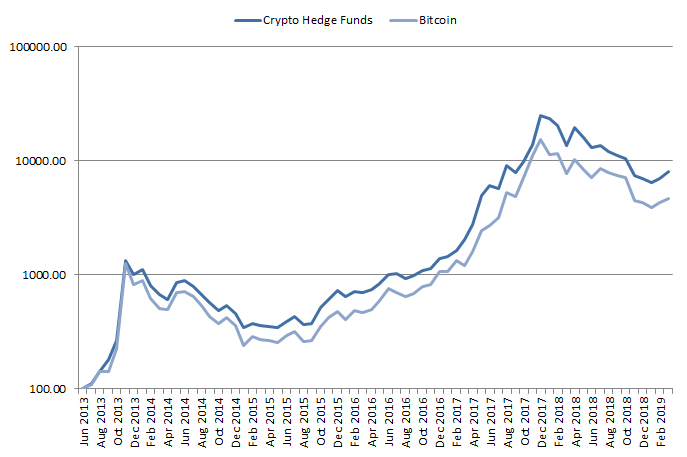

Figure 5 shows the performance of crypto hedge funds compared to Bitcoin over time. As it can be seen from it, the 2 series look very similar, posing into doubt the validity of crypto hedge funds as alpha products.

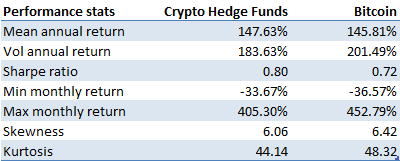

Table 1 displays the performance stats for crypto hedge funds compared to Bitcoin. As the table shows, the 2 products present very similar characteristics, with both similar returns and volatility.

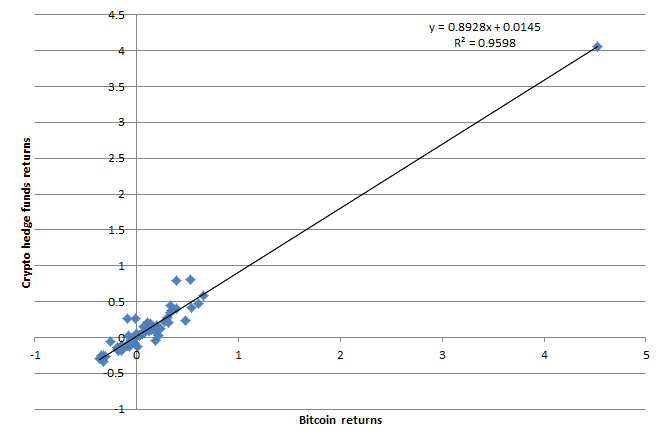

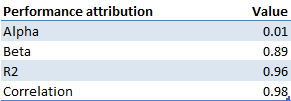

Figure 6 shows the relationship between Bitcoin returns and crypto hedge funds, while Table 2 quantifies it with a linear regression analysis. As it can be seen from them, crypto hedge funds are actually beta providers instead of alpha products as they should be. Their beta is actually 0.9, alpha is quite small (0.01) compared to their beta, and correlation with the crypto market 0.98. This is what should be expected by a mutual fund or crypto index fund offering some kind of exposure to the crypto market to its investors. These products are usually cheaper than hedge funds structures, since they do not require expensive resources spent for active management of the fund.

In the next section we analyze the performance a hypothetical systematic long/short crypto investment strategy, a possible crypto hedge fund strategy, and see if it delivers alpha as should be expected, contrary to the previous analyses.

Performance attribution systematic long/short crypto investment strategy

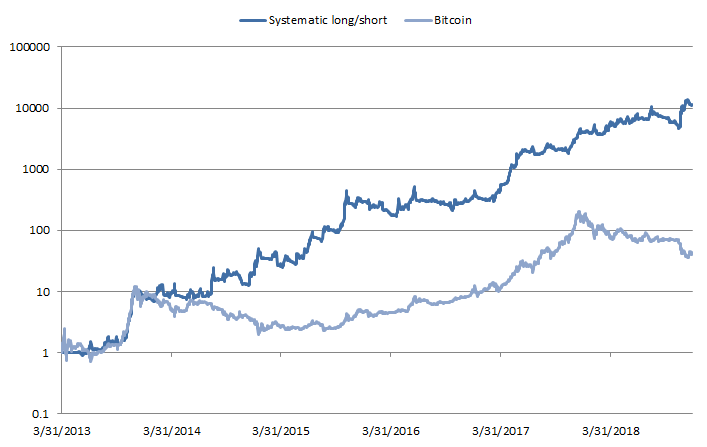

Figure 7 shows the backtested performance net of transaction costs of a hypothetical systematic long-short crypto investment strategy applied to the top 14 cryptocurrencies by traded volume. The strategy is compared to a passive buy-and-hold investment in Bitcoin. As it can be seen from the figure, the strategy would have achieved a better performance compared to Bitcoin, which is also consistent across both bull and bear markets. This is what it should be expected from a hedge fund strategy, in other words delivering uncorrelated positive returns irrespective of market conditions.

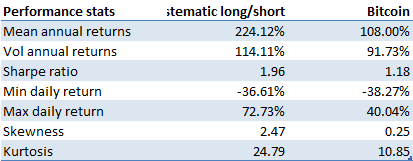

Table 3 shows the performance measures for the hypothetical systematic long/short crypto strategy and compares it to a passive investment in Bitcoin. As the table shows, the systematic long/short would have outperformed a passive Bitcoin investment. On the return side, it would have achieved an annual average return of 224%, almost double both Bitcoin. On the risk side, it would have had slightly more volatility than Bitcoin. As a result of the better return delivered with around the same amount of risk, the strategy would have achieved a much better Sharpe ratio of 1.96, compared to 1.18 for Bitcoin.

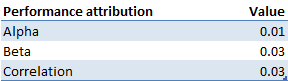

Table 4 shows the performance attribution stats for the hypothetical systematic long/short crypto strategy compared to Bitcoin. As it can be seen from the results, the strategy would have delivered real positive alpha. In fact, both beta and correlation with respect to Bitcoin returns are almost 0, as it should be expected for an alpha investment product like a hedge fund.

In conclusion, based on the previous results, a hypothetical systematic long/short crypto investment strategy would have delivered alpha instead of beta and is therefore a good candidate as a proper crypto hedge fund strategy.

Conclusion

Based on the previous analyses, we can derive the following key takeaways:

- Many crypto hedge funds launched in the past 2 years: thanks to the rise in cryptocurrency price, many cryptocurrency funds launched in 2017 and 2018. They also managed to increase their AUM in 2018 despite a bear crypto market.

- Crypto hedge funds deliver beta instead of alpha: cryptocurrency hedge funds display almost the same performance to the price of Bitcoin, having beta near 1, alpha near 0, and correlation of almost 1. This shows that crypto hedge funds are actually delivering beta instead of alpha, which is what instead their investors are paying for.

- Systematic long/short crypto investment strategy represents a possible crypto hedge fund strategy by delivering alpha: an investor considering an allocation to a crypto hedge fund should only pay for alpha instead of beta. This is for example provided by a systematic long/short crypto investment strategy, which would have hypothetically delivered uncorrelated returns to the crypto markets (alpha) in the analyzed period instead of beta.

Subscribe to our newsletter to receive our latest insights in quantitative investment management. For more info about our investment products, send us an email at info@blueskycapitalmanagement.com or fill out our info request form.